CoBuy Bay Area Housing Market Update – Dec 2018

“Those who have knowledge, don’t predict. Those who predict, don’t have knowledge. “ -Lao Tzu

So long, 2018.

The curtain is closing on 2018, and it seems everyone has something to say about the housing market. Real estate reporters, social media soothsayers, and industry incumbents are all busy making predictions. Tis the season to make forecasts! It certainly makes one wonder.

Disclaimer: I do not have the winning lottery numbers, and I won’t do that here. Instead, I’d like to cover some of the key trends, data releases and macro developments that are likely to drive the market going forward.

At CoBuy, we help folks buy and own homes together, intelligently. We are not in the business of convincing anyone to buy a home. We work with folks who want to co-buy homes to do it more efficiently and, well, better. Our fundamental view is that better information enables better decision-making.

The big picture looks decent

The U.S. economy has performed well in 2018. GDP grew at an annualized 3.5% in the third quarter, unemployment is near its 50-year low, and we have experienced a period of strong wage growth. If the national labor market is strong, the labor market in the Bay is stronger. The region continues to experience job growth despite being at (or above) full employment. This trend looks likely to continue. And Bay Area residents appear to feel the love. A recent poll ranked the San Francisco Metro Area amongst the top 10 nationally to inspire economic confidence.

As we head into 2019, many economists expect the pace of national economic growth to temper but “remain strong”, though there are headwinds (geopolitics, corporate sector, trade deficit, fiscal policy, monetary policy, etc.). The Federal Reserve is expected to raise interest rates at the upcoming meeting in mid-December, and the market expects three further hikes next year. This follows a sustained run of historically-low interest rates which has fuelled the housing market and the broader economy. The timing of monetary tightening will be subject to domestic and global economic developments, of course.

Housing markets are normalizing

It’s been a good year for most homeowners in the U.S. Nationally, home values are up 7.7% over the past twelve months. We are now seeing a rebalancing of the supply-demand dynamic in many metro housing markets across the U.S. The latest national data shows existing home sales up 1.4% month-on-month, though the annualized rate is down 5.1% from last year (source: National Association of Realtors).

Rising mortgage rates are clearly feeding a cooling off in the housing market. In 2018, the average rate on a 30-year fixed rate mortgage has risen from 3.95% to 4.81%. As one might expect, the number of folks applying for mortgages has decreased as the cost of borrowing has increased. Future interest rate hikes are likely to reduce demand from prospective homebuyers as the cost of borrowing rises. This means that some folks who might have otherwise decided to buy a home will defer that decision, either voluntarily or necessarily. Many renters who would have transitioned from renting to homeownership will remain renters by necessity.

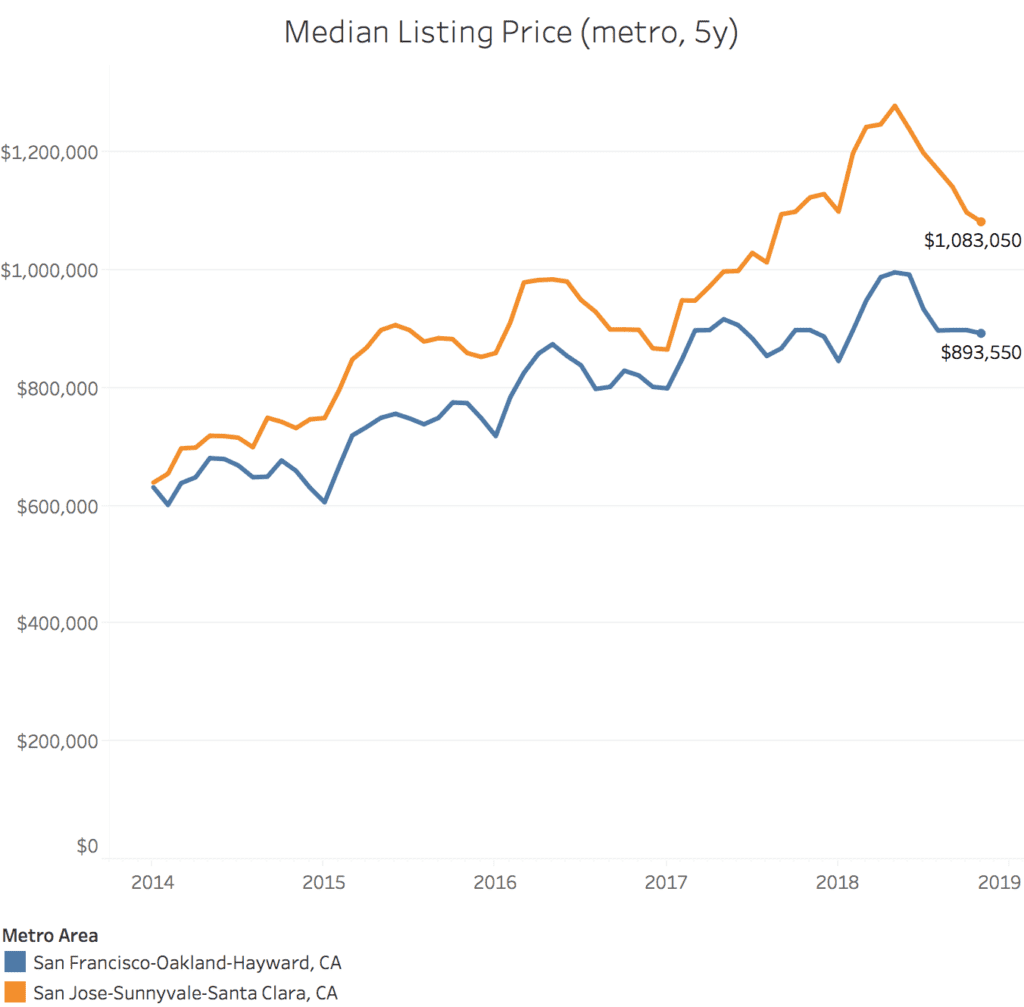

Stabilization of markets around the Bay

In the San Francisco Metro Area, home values are up nearly 10% over the past twelve months and roughly 50% over the past five years. Note the difference between “listing price”, “sale price”, and “home value”. A home isn’t necessarily sold at the listing price: often times the sale price is above or below the listing price. Home value indices are constructed in the aggregate and sometimes fail to reflect the distribution of price points of homes sold in any given month. Add into the mix seasonal swings and it becomes clear that data needs to be evaluated in context and with regard to the construction of the data set.

Data sets sourced from Realtor.com Market Data

The rapid appreciation of home prices in the Bay is slowing on an annualized basis, which is arguably a good thing. One-sided markets can’t persist forever. Home values in the San Francisco Metro Area are expected to appreciate a further 7% this year, which is likely to outstrip wage growth any way you cut it. CoBuy-certified real estate agent Edward Ong agrees. “The Bay Area market as a whole is seeing some settling. It doesn’t mean the market is about to crash…it just means that the market is becoming more realistic about prices while acknowledging that the Bay Area is still a place where real estate values will continue to be anchored in a strong regional economy and workforce.”

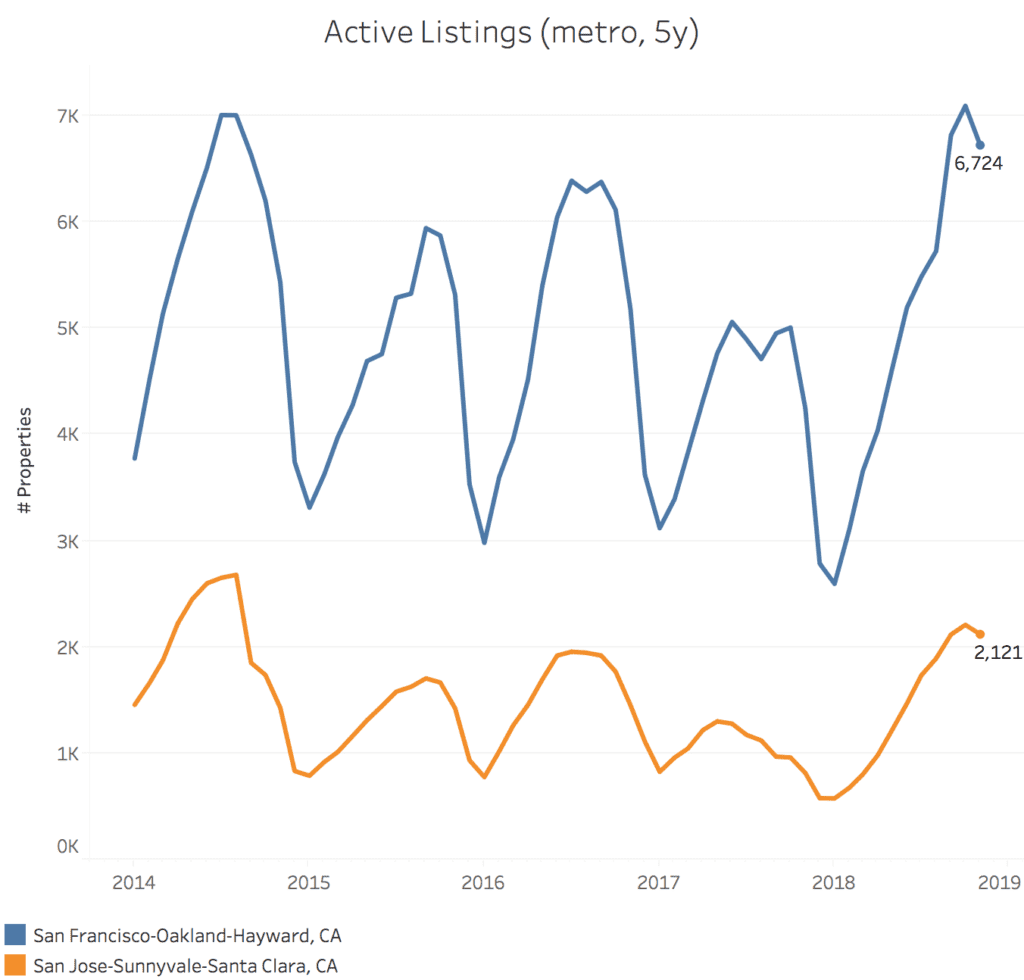

Turning to the supply side, overall inventory of homes on the market has increased notably.

Datasets sourced from Realtor.com Market Data.

Homes are now on the market an average of 38 days in the San Francisco Metro Area and 39 days in the San Jose Metro Area, both peaks for 2018. But a relatively higher inventory this time of year is to be expected. We typically see a similar seasonal movement when we look at a five-year time horizon.

Datasets sourced from Realtor.com Market Data.

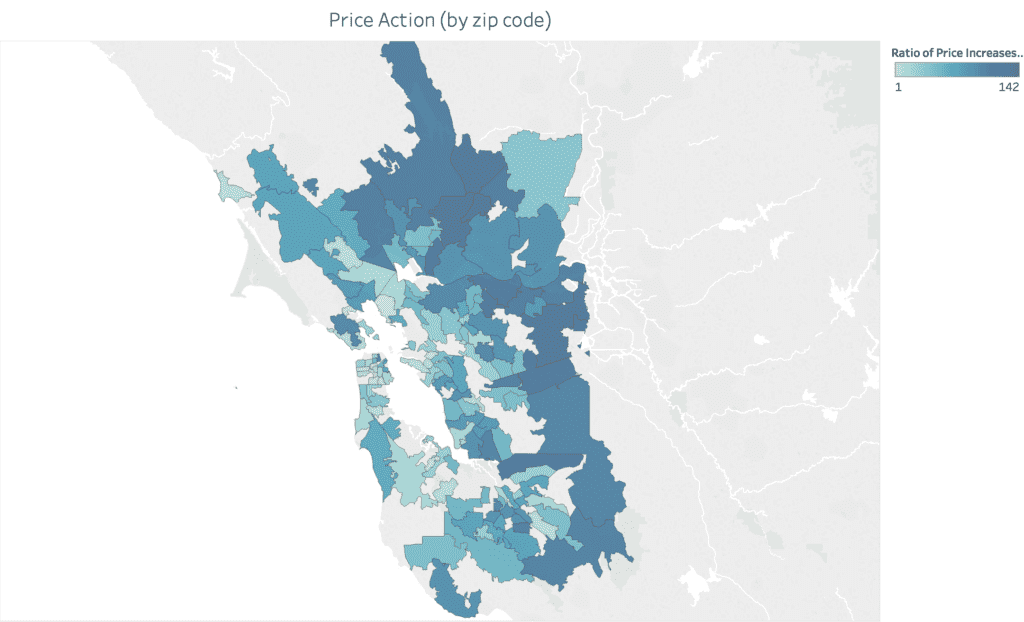

As supply increases and the supply and demand dynamic rebalances, we are seeing hyper-local price action. The heat map below ranks zip codes by the ratio of increases to decreases in listing price last month. The light blue indicates a zip code ranked higher: it had relatively more increases versus decreases to listing prices in relation to other zip codes.

Datasets sourced from Realtor.com Market Data.

Announcements of new development projects and corporate campuses are likely to impact demand in local markets. Principal Broker and Attorney Ong agrees.

“Development projects in all parts of the Bay Area will continue to bolster this region’s real estate values. The South Bay has the new Google campus in San Jose, San Francisco has the new Chase Center and its commitment to Mid-Market, and the East Bay now has the Howard Terminal project. All of these will add value to current real estate projections and the economy at each local level.”

Co-buying means more bang for your buck

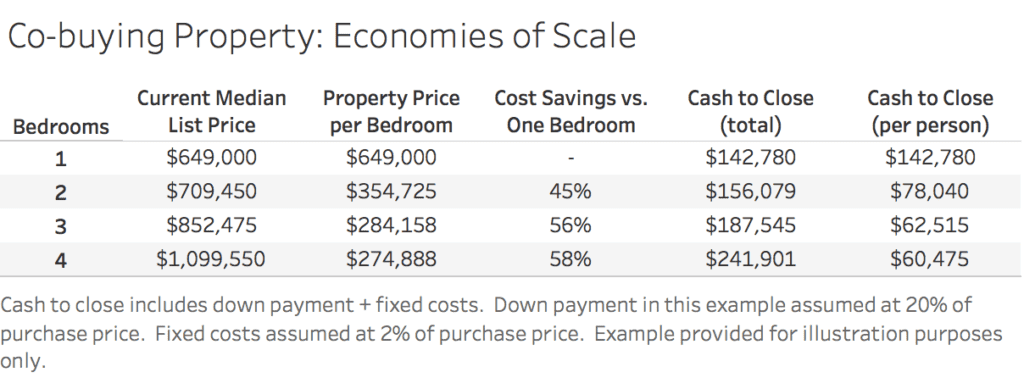

Like buying in bulk from Costco, buying a larger home is relatively cheaper on a per-bedroom basis than buying a one-bedroom home. Nowhere is this more evident than around the Bay. On a per-bedroom basis, a three-bedroom home is 56% cheaper than a one-bedroom home in the San Francisco-Oakland-Hayward Metro Area. Economies of scale are real, and combined purchasing power means more bang for your buck and greater optionality in terms of access to housing stock.

To demonstrate, let’s use current median list price data from the SF-Oakland-Hayward Metro Area. In our example, we’ll assume a 20% down payment and closing costs for the buy-side at 2%. (Note: a 20% down payment isn’t necessarily required, and many borrowers qualify for low down payment mortgages).

The median list price for a one-bedroom in the SF-Oakland-Hayward Metro Area is currently $649k. In our example, a single buyer would need to bring about $143k in cash to purchase this property.

At the current list price for a four-bedroom home, four individuals could each contribute $60k in cash towards down payment and fixed costs up front. By pooling resources to jointly purchase a home, the financial hurdle to homeownership is substantially reduced.

Context is key

For anyone thinking about co-buying a home, it’s important to consider several factors:

- Motivations for the purchase

- Timeline

- Geography

- Personal finances

- Life circumstances

- Financing eligibility

- Interest rates

Decisions about if and when to buy should reflect your personal circumstances and those of any co-buyers. Let’s say I’m sure I want to buy a home within the next two years. Let’s also suppose that I decide to wait for a year to see what happens in the market. If during that twelve-month period borrowing costs increase by 50 basis points, property prices increase by 7%, and my rent increases, this could make it challenging to execute on my plan to purchase.

Considering buying a home with friends, family, or a loved one? Log on to CoBuy or get in touch. CoBuy makes it easier to buy and own a home together, intelligently.

Related Posts

Curious about co-buying?

We're here to help, seven days a week.