Renting with Friends? 5 Reasons You and Your Friends Should Consider Buying Together

So, you have a friend or friends who you know, like and trust – someone you have been renting with, perhaps? Living together is comfortable and enables you to have a place that doesn’t take too big a bite out of your paycheck each month. Still, the notion of having your own place one day is something that you hope to achieve. What if you could take a step in that direction now? What if the time, effort and cost was relatively efficient and could, ultimately, help you get to your longer term goals sooner?

Don’t let inertia keep you in a position to pay down a mortgage that is not your own. Every rent payment you make builds equity for your landlord. You are likely paying their mortgage, property taxes and insurance, and maybe some maintenance and repair costs. You may even be helping add a bit to their retirement. That’s noble! But what about you?!

Alternatives to Rent vs. Buy

You may still be paying off some student debt or saving towards a down payment for a place of your own. Perhaps you qualify for a property and may even have an adequate down payment. You just can’t afford what you want or the area you want to be. The rent versus buy decision is not a black and white one.

What if there were another option that combined some aspects of both buying and renting? What if the same group of friends or family members could reasonably pool their resources and buy a home together? It needn’t be forever. In fact, it could be a fixed term play with a timeline agreed upon up front.

By combining resources, the whole may be greater than the sum of the parts. Said another way, let’s say you are three friends and each qualify for a $300,000 loan. In your metropolitan area, there are no $300,000 properties that you would want to live in that are near desirable amenities. There are, however, $800,000 3 bedroom properties that are right where you want to be and are quite nice.

So, you could live with your friends, share ownership and the benefits that come with that, AND pay less than you are paying in rent. All this and the property is yours!

5 Reasons to Buy a Place Together

1) Stop burning money on rent and start building equity.

2) Lock in your housing cost and avoid the need to relocate at inconvenient times as rents rise.

3) Discover economies of scale. On average, the cost per bedroom of a 3-bedroom room place is 40-60% less expensive than a one bed in many major metropolitan areas.

4) Enjoy tax benefits from deductible portions of your monthly payment against current earned income and take home more of your monthly earnings.

5) Spend less of your monthly income on mortgage costs than on rents and, possibly, get more home for the same money.

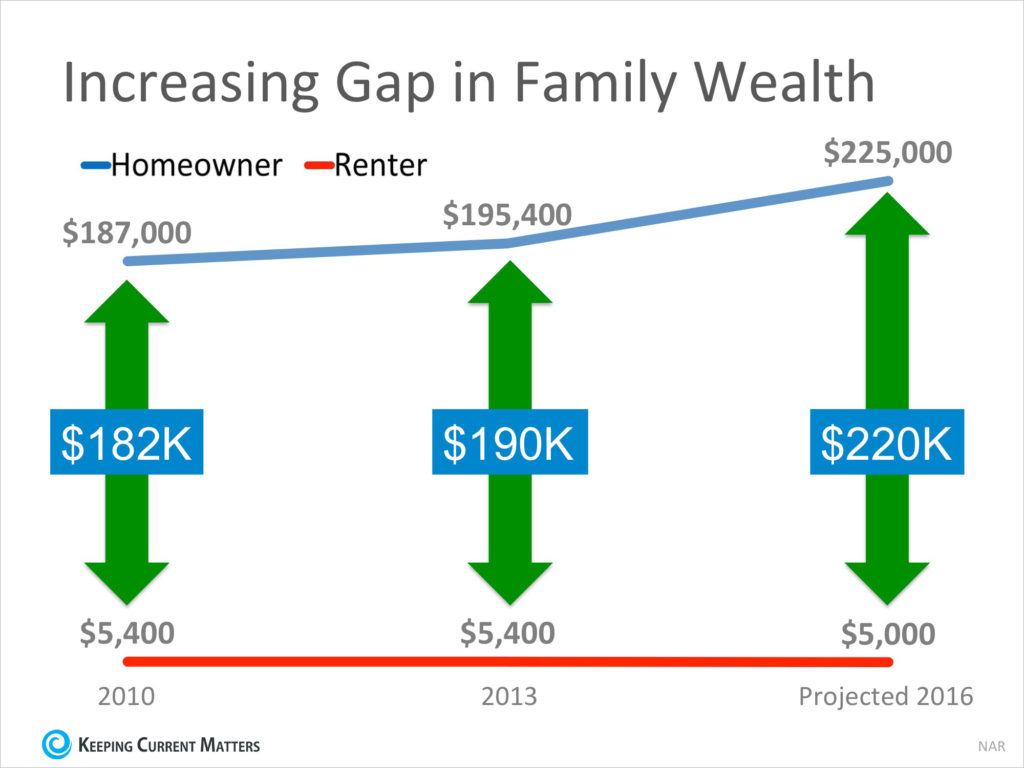

The Net Worth Effect of Homeownership

Research suggests that homeowners’ net worth is some 36X that of renters’, on average. The National Association of Realtors’ Chief Economist, Peter Yun, predicts that the Federal Reserve’s next study will show that 2016’s homeowner will have an average net worth 45x that of their renter peers.

Homes in major metropolitan areas are appreciating at higher rates than in the past. While recent appreciation is slowing from the phenomenal rates of the most recent couple of years, they are still healthy. Appreciation rates will be tempered as mortgage lending rates rise. Still 2017’s likely rate increases will still qualify as some of histories lowest rates on record. Supply of new homes will take years to catch up with the growth in demand from in-migration and organic growth in the most attractive metros.

Why the Divide Will Continue to Grow

The economics of building and development due to public policy changes, ecological protections and labor and supply costs, make building affordable entry level homes cost prohibitive in most major markets where the land prices are high and available land is scarce. Thus, building has not kept pace with demand for nearly a decade.

At the same time, millennials (those age 18-36) are aging into their home buying phases. As the largest generation on record at a reported 86 million, this segment will be the most likely to comprise the first-time homebuyer market over the next few years.

Pooling resources to buy a place now and get on the property ladder isn’t for everyone. If you are uncertain about your earning prospects or don’t plan to be in a given area for at least two years, renting may be a better option. However, for those who do want to start building their net worth and do believe they will stay in their place for two years or more, co-buying is an attractive option.

Buying a home is complex, increasingly so when multiple parties are involved. People buying together are not afforded the same protections of law as married couples. As such, it is important to understand the potential pitfalls of a joint ownership and provision for avoiding the challenges and mitigating the potential risks. Key to your education and protection is working with professionals who are adept in the nuances of a cobuy.

Bottom Line

If owning a home is important to you and you are not ready to buy what you want on your own, co-ownership may be an attractive alternative. A joint property purchase with friends or family, whether they live with you or not, may be a worthwhile pursuit. Just like renting, cobuying does not have to be forever. For more information on cobuying visit us at goCoBuy.com or send us a note at info@gocobuy.com.

Related Posts

Curious about co-buying?

We're here to help, seven days a week.