CoBuy vs Renting: The Basics

Co-buying vs Renting

S o you’re tired of getting spanked by ludicrously high rents that seem to just keep going up? We hear you. But just how does co-buying stack up versus renting? Several factors make this comparison challenging. First, it can be tough to put a dollar value on subjective notions like homeownership or flexibility associated with renting. As individuals, we are likely to value these things differently. Some people have a strong desire to own their own home while others prefer a change of scenery every year. The second factor that complicates a cost-benefit analysis between these two options is the uncertainty surrounding the housing market. Sure, if home values are certain to appreciate year after year then all else equal many people would want to own (or co-own) a home. The opposite would be true in a market where home prices are certain to fall. It follows that if you really want to compare co-buying to renting, you might take a market neutral approach where home prices are flat or appreciating in line with inflation.

Here are three points worth considering when weighing up co-buying vs. renting:

On average, first-time owners in Seattle spend less on their mortgage payment than renters spend on rent.

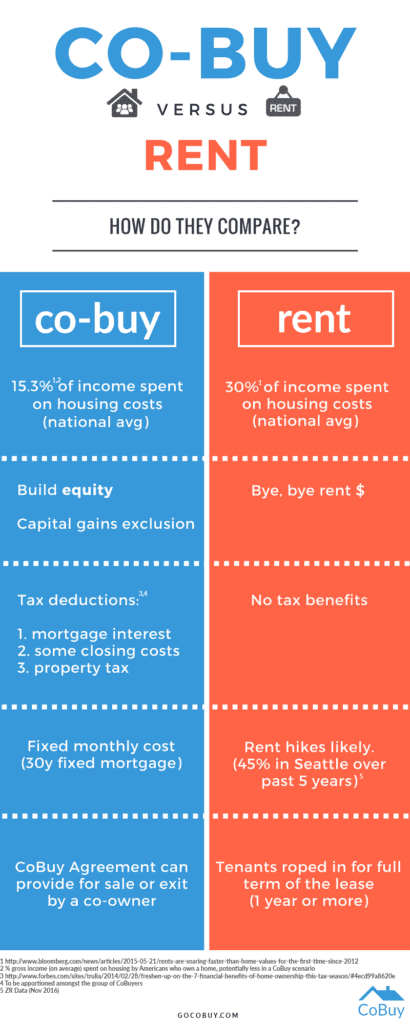

According to Zillow data from April 2016, the average first-time home buyer in Seattle spends 22.7% of their income on mortgage payment while the average Seattleite renter spends 31.2% of their income on rent. Nationally, this discrepancy is even higher with renters spending roughly 30% on rent while mortgage holders spend 15.3% on housing.

CoBuy boasts financial incentives that renting doesn’t.

When you co-buy, every month a portion of the mortgage payment goes towards paying down the principal owed on the home loan and co-owners build equity in their home. Think of this as a kind of automatic monthly savings system. Co-owners also benefits from tax deductions: they are eligible to write off interest charges and certain expenses against their taxable income (interest paid on their mortgage, part of their closing costs on the purchase, and a portion of their property tax). And while we take a “market neutral” approach with regards to property values, it should be noted that if the home does appreciate between when the co-owners buy and when they sell, the co-owners would benefit from up to $250k capital gains exclusion (so if you bought a house for $500k and sold it for $600k, this $100k capital gain is tax free).

Joint ownership can reduce the uncertainty associated with rent increases and forced moves.

When you co-buy a home and lock in a 30y fixed-rate mortgage, you drastically reduce uncertainty around your monthly housing spend. Unlike rents in Seattle, your mortgage payment won’t magically increase by $1,000 per month from one year to the next like some Seattle rents. What’s more, interest rates remain near historic lows, which means some people may be tempted to pull the trigger on joint home-ownership to take advantage of this low rate environment. As any mortgage calculator will show you, a small increase in rates can have a substantial impact on the total interest to be repaid over the full life of the loan. Finally, when you co-own a home there is no landlord to inform you the property has been sold and you have to move at the end of your term. With the average cost of an in-state move $1,170, you’ll have enough to stock the fridge and throw a few shindigs in your new place.

C o-buying isn’t a “one-size-fits-all” solution and when buying a home alone or with others, there are many important factors to take into account. Due diligence and a thorough understanding of your finances is critical and you should engage qualified professionals in lending and real estate who have experience with the ins and outs of co-buy transactions. For those thinking about co-buying a home, CoBuy can help answer questions and fill in the blanks. There are some things in life you shouldn’t do unprotected, and co-buying a home is no exception.

Related Posts

Curious about co-buying?

We're here to help, seven days a week.